Samuel Heath & Sons plc (HSM): A Nano-Cap Manufacturer of Luxury Bathroom Fixtures with a 35-Year Track Record of Profits and Why I'm Passing on It

The tiniest UK company I've ever seen at this level of profitability and consistency at £7.8m market cap.

The markets have been turbulent this week, which means Mr. Market may soon be knocking at the door with a great offer. Hope everyone is looking for bargains out there. I have a quick write-up on another UK stock here as a result of my UK A-Z process which you can read here.

I often come across stocks that look appealing at first glance, but as I dig deeper, the picture becomes less convincing. Despite this, I still find it beneficial to write up my findings, as the research itself offers important lessons and helps refine my investment thinking even if I don't end up taking a position. I also enjoy writing about obscure stocks like these, so much of investing discussion has revolved around the same 50 names you hear all the time, there has to be someone who's interested in a £7.8m British manufacturer.

Background

Samuel Heath & Sons plc (HSM) is a closely held nano-cap manufacturer and distributor of luxury bathroom fixtures for wealthy homeowners. They are based in Birmingham, UK where they operate and run their only facility. They have a UK showroom in Chelsea and a US customer services location in New York City. They have around 110-120 employees at their company, most of them are involved in the manufacturing of their products. The company was founded in 1820 and held within the Heath family at least since the 1950s, it's not clear if this company was under a different name or family prior to that.

As you can see below these are some really pricey bathroom fixtures. You aren't going to find these are your local Home Depot or hardware store. They also have a case studies page with some images of their products in some of their client's homes.

Source: Link

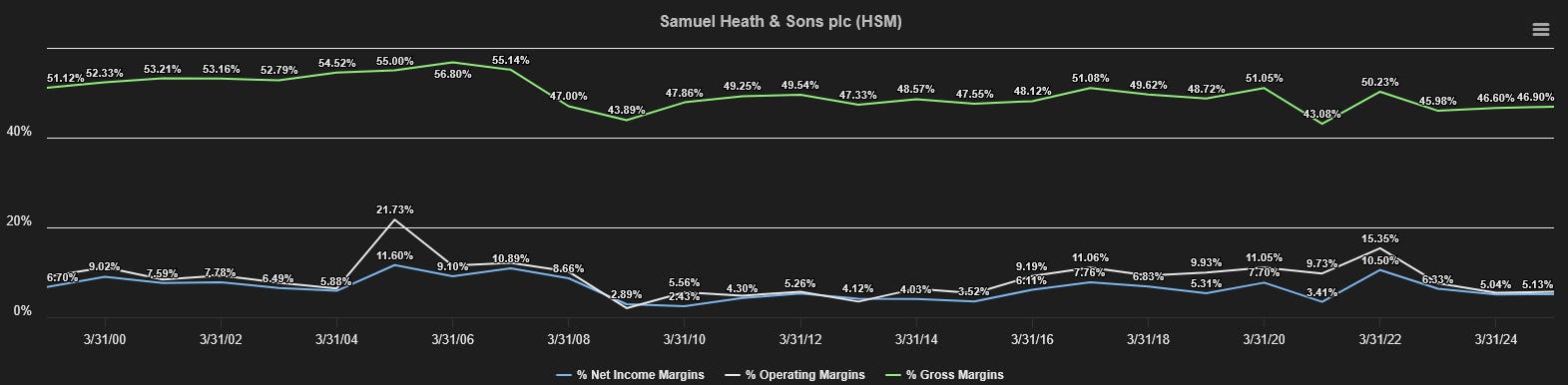

In the last couple of years about 50% of the revenue is derived from the UK and 50% from overseas customers which I imagine is predominately the US but they don't really say. None of their customers account for 10% of sales or more. In general over the past 20 years, the company goes through cycles of higher margins and cycles of lower ones:

Source: Tikr

It is very impressive seeing a company of this size being able to generate over 35 years of reported earnings with no losses.

Source: Tikr

Business Figures & Ratios (4/3/2025):

Market Cap: £7.84m

Price: £3.10

P/E: 10x

P/TBV: 0.75x

P/NCAV: 1.36x

ROTCE: 6.26%

ROE: 6.24%

Z-Score: 5.17

Closely Held Enterprise: Low Information Stock

This is a pretty low information stock, not surprising at its market cap size. I've tried to learn about the business, its history and the history of the Heath family and it's pretty obscure. There's not much you can uncover about this company off of the annual reports either, things I've looked for to no avail:

Business Summary/Detail

Sq. footage of their PP&E

Inventory detail beyond stages of production

Who their customers are or a general idea of who they target

If they utilize a supplier or a middle man

Without an answer or a good educated guess on these items, figuring out this business and trying to come up with an appraisal value seemed very difficult. This company basically acts like a private business in many respects given how bare some of this information is on their annual reports.

For anyone who's interested in this stock or interested in the future it may be worth getting a list of questions and sending them in to their finance director who runs their IR page. I was considering it but given that I'll be passing on it, I'll be respectful here and not waste their time.

Illiquid Stock

This stock is pretty illiquid where insiders own about 79% of the stock although taking a count from the ownership information from Tikr summed up, it could be as much as 85-90% of the shares are locked up by long-term holders. Shares turnover at a very low rate at about 1% per year (24k shares traded last 12 months / 2.5m shares outstanding = 1%) and the stock has a beta of 0.07.

If you are running a diversified portfolio you shouldn't have trouble accumulating enough shares for a decent position however at 24k shares trading in the last 12 months that could mean you could only accumulative ~£77k worth. Can you accumulate more than 24k shares? Possibly, you never know unless you put the bid out and see if it gets filled. Additionally, if you are having trouble getting shares you can put orders in around times when the company issues their mid year & annual reports you may have better luck since Mr. Market likes to buy and sell off of the announcements.

Pensions

The company has an employee pension plan that it contributes to. Historically it was in a deficit for a number of years but the company has made significant contributions to it to clear the deficit. In the last annual report, the chairman's letter has discussed a potential pension buyout plan. Pension contributions in 2024 were around £870k, contributions for 2025 will be around £300k.

Quite frankly I'm not sure what this pension buyout will entail, I think this is something I'm not familiar with and would have to research this in depth to understand if this could potentially mean more cash would have to be tied up in seeing these buyouts through or if there's enough invested in the pension plan to buyout members. They did just get out of a pension deficit and now have £767k in retirement scheme assets on the balance sheet.

The pension contributions have ate away at FCF causing large differences between earnings & CFO as well as FCF. It's a big problem in trying to understand where your returns come from and trying to appraise the stock because your owner's earnings or FCF is much less than reported earnings.

Source: Tikr/Own Calculations

What I ended up doing is just backing out the pension contributions to see what the FCF numbers could theoretically look like over the last couple of years if the pension plan didn't exist. It ends up smoothing out those EPS to FCF conversion rates quite well. It ends up being a difference from earning £7.5m FCF vs £3.25m. Unfortunately this isn't the reality here, there will be some amount of the pension contributions that will hit CFO until the buyouts are worked out. In the meantime the company deciding to fund the pension will lower returns, and the company deciding to fund less of the pension will increase returns, viewing it like debt in a way.

Why I Am Passing on Samuel Heath & Sons?

There's a number of reasons why I am passing on this idea, I poked holes in this idea and in the end it seemed like there were too many questions, not enough answers and not cheap enough. Some of the reasons below, by themselves perhaps it wouldn't be problematic but all in aggregate makes the idea less attractive for me:

Insider controlled company of a sub-par business, meaning very low chance of someone to take it over nor would you want to earn the poor returns while you wait.

1% share turnover and 80-90% shares locked up long-term meaning stock buybacks are unlikely, nor do I think the company would ever do it based on their capital allocation history.

Some of the questions previously discussed I couldn't answer from reading through annual reports and basic company research.

Low earnings quality due to pension contributions/obligations

Don't have good working knowledge on how the pension buyout will play out

Unsure if this business can earn its cost of capital, ROE has been around 6-8%

Don't have a good way to determine an earnings based appraisal value

Book value contains a lot of inventory and PP&E. Did a quick liquidation analysis below.

Source: 3/31/2024 AR/My Own Calculations

Notes on the follow assets:

Receivables at 71.5% - as it includes only current receivables

Inventory at 50% - A complete guess, I'm not sure what you can get for expensive luxury bathroom fixtures in a liquidation sale.

PP&E at 100% - It seems like the company does book revaluations for their PP&E done by a valuation specialist. The big one I was looking into was the manufacturing facility in Birmingham which is around £1.7m per the annual report. No idea on the sq footage, tried to compare what was around the area and running a grok/chatgpt prompt to get an idea and it seems like £1.5m - £2m is a decent estimate. To be honest using 100% of the value is probably not right but by that point it was obvious that on a liquidation basis it's already too expensive.

On a liquidation basis I got £1.09 per share on a £3.10 stock price which is just much less attractive vs it's book value.

Conclusion

This stock looked attractive when publishing my UK A-Z list but as I dug into the numbers there was very little that I actually like in this idea. It's a good reminder how sometimes book value can be very deceiving until you verify the quality/value of those assets yourself. On liquidation basis the stock is unattractive, on earnings basis I don't have a good idea to estimate an appraisal value on the stock. A lot of the general catalysts for something like this seem less likely. Although it is an illiquid stock which can be beneficial to hedge some of the crazy volatility in the markets as it won't trade often but returns will be lacking here. Outside of reporting good results, it seems like the stock may be dead money for a number of years.

Disclosure: No position, I am not short on any securities mentioned in this post.